Do you know if your business is cash or accrual basis?

I wrote this article years ago and never published it. For many, this is a confusing topic and I wasn’t sure if I would confuse the reader even more. To try to prevent this, I have split the article into two sections. If you just need to know the bare minimum you can stop reading after section one. If you need all of the details or just find the topic fascinating, then you can read to the end of section two.

Section One: The Bare Minimum

What is cash basis accounting?

Cash basis accounting is pretty straight forward.

With this method, funds received and funds paid out are recorded at the time the funds physically move.

There are no adjusting entries to set up – no AR (accounts receivable) or AP (accounts payable). Many small businesses use this method for its simplicity.

As a side note, businesses required to follow GAAP (Generally Accepted Accounting Principles) are required to use Accrual basis.

What is accrual basis accounting?

Accrue means to accumulate. Accrual basis accounting is used to properly match expenses and revenue to a specific time period. It’s known as the Principle of matching cost and revenue.

What does that mean?

In this method, revenue is recognized when earned and expenses are recognized when incurred.

In this method, Accounts Payable (AP) and Accounts Receivable (AR) accounts are used.

What does that mean for your business?

AR is used to accrue income. For most small businesses, this means invoices are set up. An invoice is by nature an accrual entry. (For you, an invoice means that someone owes your business money.) Money has not been received, but has been recognized by having completed a job, sold a product, or the like.

AP is used to accrue an expense. For your business, this might mean you set up a bill. A bill by nature is an accrual entry. Money is due to another party, but you have not paid it yet.

Section Two: Details With Examples

What is cash basis accounting?

Cash basis accounting is pretty straight forward. With this method funds received and funds paid out are recorded at the time the funds physically move. There are no adjusting entries and AR and AP are not used.

The entry when revenue funds are received:

Debit Cash/bank account

Credit Revenue

The entry when funds go out to pay for an expense:

Debit Expense account

Credit Cash/bank account

When you compare these entries to the final result entries on accrual accounting (below) you can see that the final entries are the same.

Sometimes an expense is incurred in one period and paid in a subsequent period. With accrued basis, the liability is set up to recognize the expense in the period it is incurred. Think of it as an expense you have committed to but haven’t paid the corresponding liability. Accrued expenses are recorded with an adjusting entry to set up the liability.

An expense accrual example for a company with a fiscal year-end December 31:

On January 10th a payment request is received for a product or service you ordered and received in December. Since the liability was incurred in December you will need to account for it with an adjusting entry in December. This will allow the expense to show in the proper year regardless of when it is paid.

To book an ‘adjusting entry’ you will need to set up an AP item.

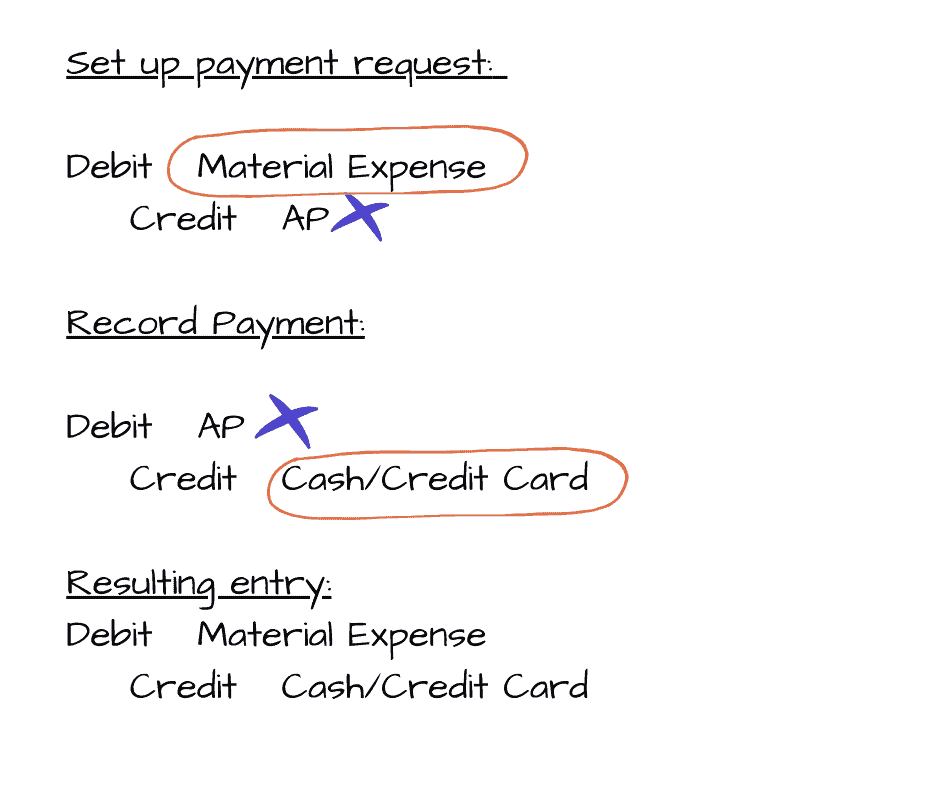

For example, the above expense is for material, the entry to set up the payment request is:

Debit Material Expense

Credit Accounts Payable

The entry when the item is actually paid:

Debit Accounts Payable

Credit Cash/Credit Card

When multiple entries are used to book one item, I like to look at the entries and isolate the resulting factor.

In the example above, you can see that the second entry reverses the AP account, which reduces the liability.

The two entries left on the books – Debit to material expense and a Credit to Cash/Credit Card.

Think of the AP account as a holding account.

If you are using accrual basis and an accounting system, you might not think of setting up an AP item as an ‘adjusting entry’, but that is actually what it is. In an accounting system, the most common way to set up AP is by entering a bill. The AP account is offset in the background of the accounting system.

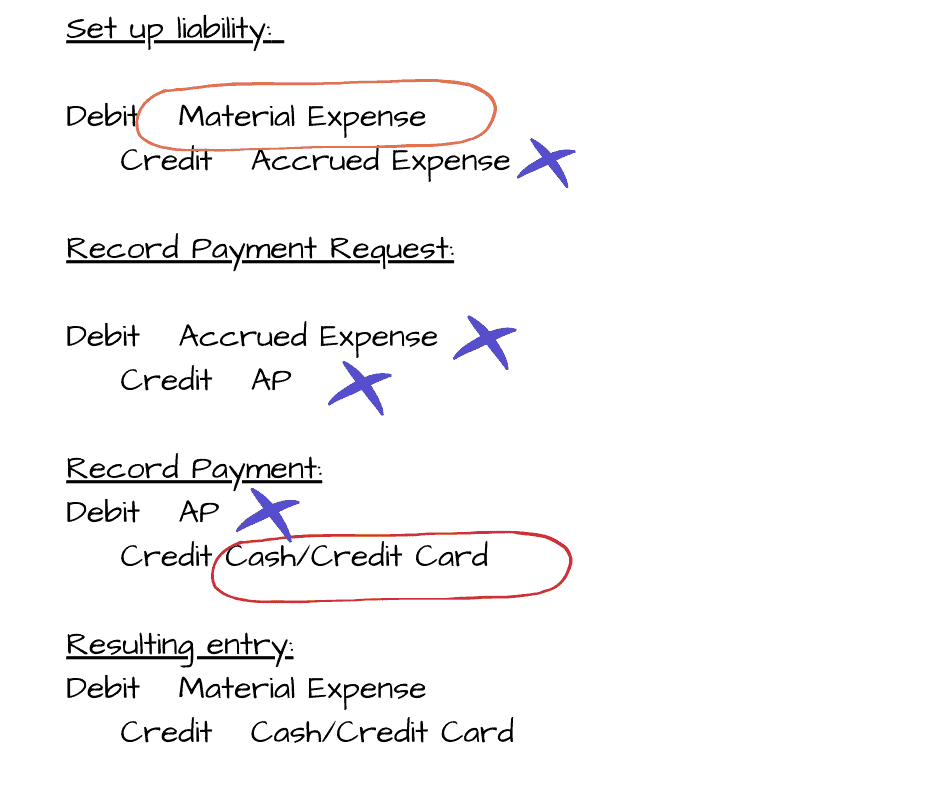

You can also accrue for expenses that you are aware of but have not received a request for payment yet. In the scenario above, the expense can be booked in December when the materials are received but before the request for payment. In this case, the company might decide to set up an account on the chart of accounts labeled ‘accrued expenses’ to track this type of expense. One reason, generally the main AP account is not used until a request for payment has been made by the vendor.

The entry to set up the liability:

Debit Material Expense

Credit Accrued Expense

The entry when the payment request is received:

Debit Accrued Expense

Credit Accounts Payable

The entry when paid:

Debit Accounts Payable

Credit Cash/Credit Card

We can look at all three of these entries and isolate the end result.

Entry two reverses the accrued expense and sets up AP. Entry three reverses the AP account and books cash.

The final result from the three entries is a Debit to Material Expense and a Credit to Cash/Credit Card.

Now let's look at accrued revenue:

Accruing revenue recognizes income in the period when it is earned even if funds haven’t been received. It’s like providing a product or service on credit. It is necessary to record the amount owed to your business in the corresponding AR account and track who owes your company money and for what. For example, some service companies do not require payment until the service is complete. Once the job is complete, they will then invoice the customer for the completed work. For the service company, the revenue has already been earned it just hasn’t been received from the customer, because it hasn’t been invoiced.

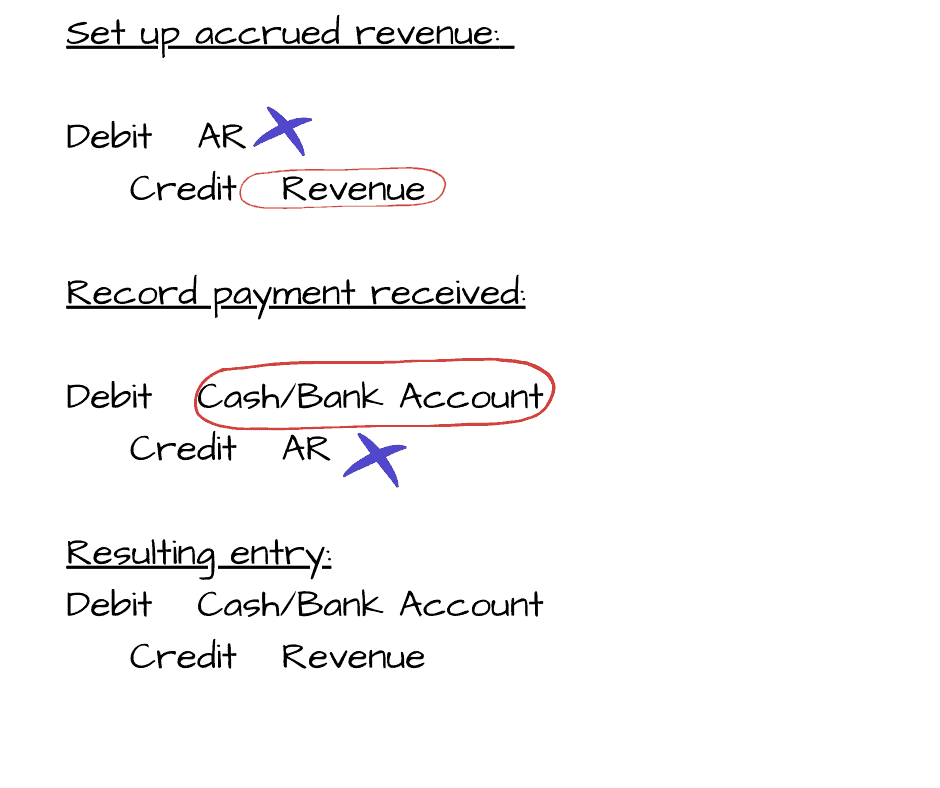

For instance, ABC company provides consulting services to company A during March and completes the engagement on March 25th. As of March 25th, the revenue has been earned for ABC company. At this time, ABC company can accrue for the revenue on their books. They do this by setting up an AR entry to record the funds owed to them. As well as, setting up the customer that owes and the service provided. The most common way to do this in an accounting system is to set up an invoice. In an accounting system, the AR account is booked in the background, so you may not ever need to select this account in an entry.

To see the flow of the entry to set up accrued revenue see below:

Debit AR

Credit Revenue

The entry when the payment is received:

Debit Cash (bank account)

Credit AR

When we look at these two entries together we can see entry two reverses the AR account. Which leaves a final entry as a Debit to cash and a credit to revenue.

Think of the AR account as a holding account.

How often should you book accrual entries?

Businesses can book accrual entries monthly, quarterly or at year-end. The determination is company specific and is based on financial reporting requirements. If accruals account for high dollar volume throughout the year, it is beneficial to record the accrued adjusting entries monthly or quarterly. This will allow the financial statements to correctly reflect the liabilities and assets throughout the year. If the amount is immaterial, it might be ideal to just book the adjusting entries in the last period of the fiscal year. This will properly account for the expenses and revenue in the correct year.

If your company sends invoices to customers to request payment, this should be done routinely.

To recap, think of accrued expense as a product or service you have received but haven’t paid for. And accrued revenue as income you have earned but haven’t received yet.

That's it, you made it!

If you are reading this conclusion, you made it through the entire post. Congratulations! I hope you learned something new and aren’t more confused now than before. If you are, I recommend you think about an example of when your company would need to accrue an expense or revenue and write down the entries that would correspond. Use the example entries as your starting point. Also, think in very simplistic terms that accruing is the act of setting up AP and AR.

If this article was helpful, leave a comment. To learn more on small business topics be sure to check out our guidebook, “Becoming a Sensible Business Owner”. It includes 40+ pages helping business owners set their business up for success!

~ Brandon & Christi are successful business owners who enjoy traveling and making a mess in the kitchen with their two daughters.

The article is for informational purposes only and should not be construed as business, accounting, tax or legal advice. Details are subject to change without notice.

Each business’s tax situation is different, so be sure to consult with your tax professional on your specific tax plan.