There are many bookkeeping tasks that should be performed routinely. One of the most overlooked of them is account reconciliation. Account reconciliation is when the transactions and ending balance on a bank or credit card statement are compared to the transactions in an accounting system.

RECONCILIATION PREP:

Before an account can be reconciled the below need to be completed.

Sales & deposits are entered into the accounting system

Expenses are entered into the accounting system

And then at the end of a statement period, accounts are reconciled.

WHY RECONCILE?

Reconciliation is the process used to determine the accuracy of recorded transactions.

Below are instructions to reconcile accounts in an accounting system, such as QuickBooks:

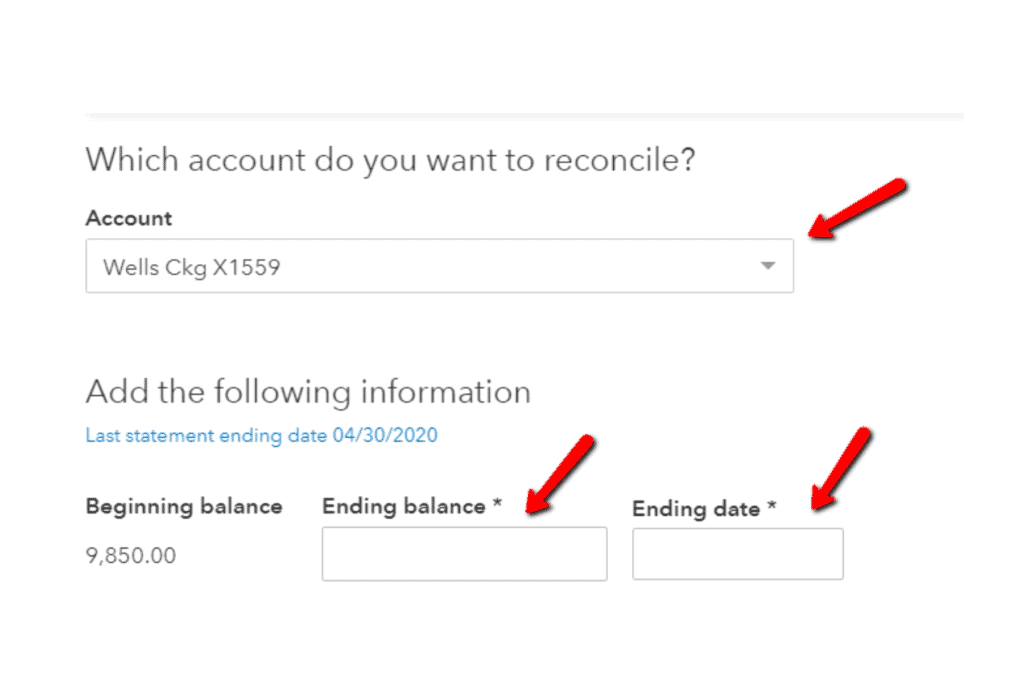

1. In the reconciliation module select the account to reconcile. Enter the ending statement balance and the ending statement date. (See picture one below.)

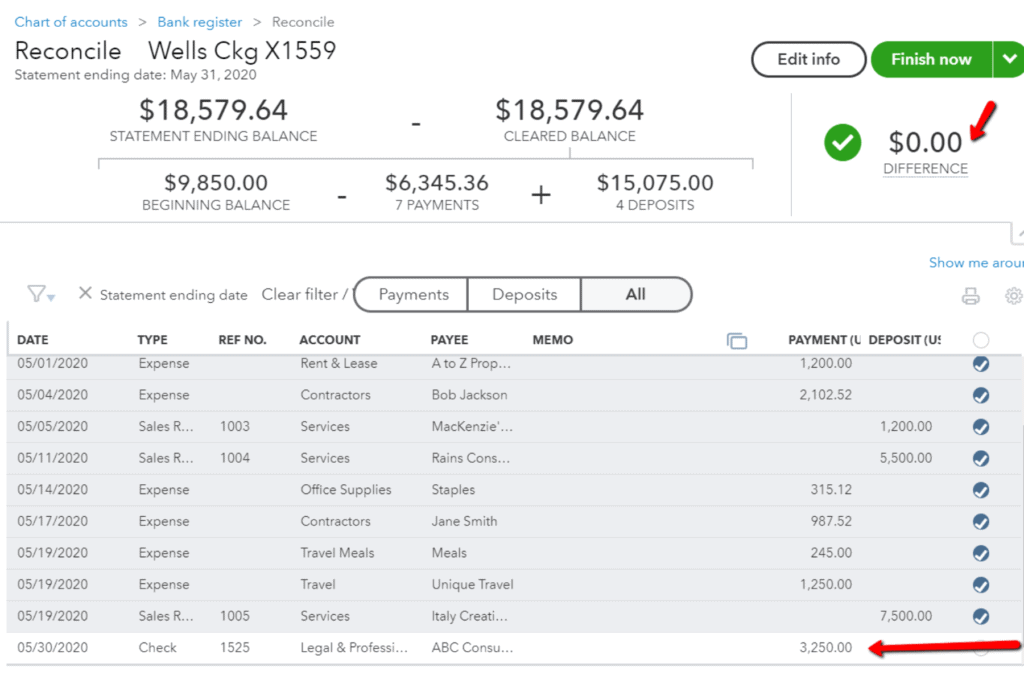

2. Look at the transactions on the statement and check each off on the reconciliation screen. In picture two below, all of the transactions on the statement have been marked off. There is one item not on the bank statement. See #4 for how to handle it.

3. Circle any transaction(s) on the statement that isn’t on the reconciliation screen (if any). – Determine why these aren’t in the system and enter them.

4. Look at the transactions on the screen and determine if there are any not checked off, which means you did not see them on the statement. – Determine why these are in the system and not on the statement. If they are duplicates, delete them. If there are transactions that haven’t cleared the bank yet but will, leave them unchecked. An example of this is an outstanding check. (An outstanding check occurs when you wrote someone a check and they do not cash or deposit it by the end of the month.) Another example is a deposit that hasn’t settled at the bank. If you deposited money in the bank on the last day of the month it might not clear until the next month. Which would mean the deposit was in transit or outstanding.

In the second picture above, there is one item not on the bank statement. It’s the item not checked off. This transaction is a check that was written on the last day of the month. It’s considered outstanding or in transit since it hasn’t cleared the bank. We will leave it on the screen unchecked. On next month’s reconciliation, it will appear on the screen again. If it has cleared the bank it will then be checked off.

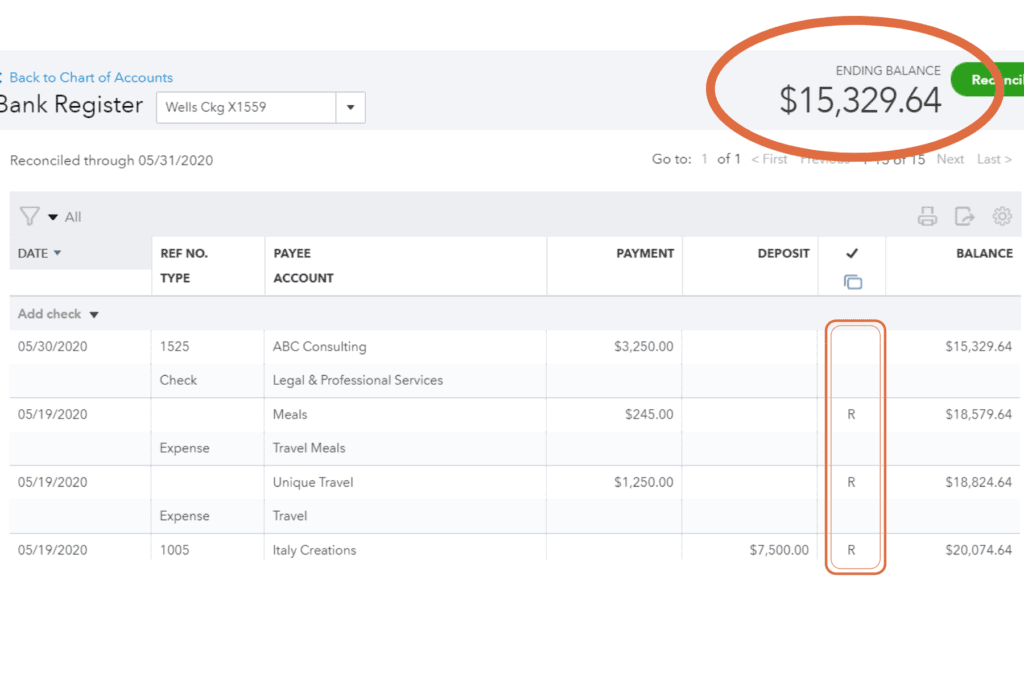

As a side note, you will notice that the bank ending balance does not calculate the in-transit items. You need to keep in mind, this check will clear at a later date and the funds are not available for use. Conversely, your accounting system check register should have an ending balance of the bank balance minus this check. In this example, it would be $15,329.64. See the picture below.

PRO TIP:

In this picture, you will notice the column labeled with a checkmark that I boxed in. This box is blank on the check that hasn’t cleared the bank. On the remaining transactions, this box has an ‘R’. The ‘R’ means the transaction has been reconciled. If the transaction had a ‘C’ that would mean the transaction was checked off on the reconciliation screen but the reconciliation is not complete. The ‘Bank Register’ in your accounting system can be a handy tool to see what the true picture is of an account.

5. When you have gone through the entire process, the reconciliation should be in balance. (See picture two above.)

You will go through this process for all bank and credit card accounts. I recommend doing it monthly. It will help with ensuring accuracy in your accounting system. That in turn results in accurate reports, such as the Profit & Loss Statement and Balance Sheet.

Also, if you have any loan accounts, such as auto loans, you will perform the reconciliation process on these as well. It’s not necessary to perform this monthly, but at the very least at year-end. This process will make sure all transactions were entered correctly and the principle and interest amounts are coded correctly.

So don’t forget to reconcile those accounts! It’s really the only way to know that what’s in your accounting system is complete and accurate.